Occupancy for the top 10 countries by total supply came in at 69.3% which was slightly higher than the aggregate of the other countries around the world excluding the U.S. (63.7%). Huge recoveries can be seen across many of the countries that last year had restrictions in place.

U.S. Performance

U.S. hotel industry occupancy plateaued at 65.1%, basically matching the level achieved the week prior (65.2%). While average occupancy did not change, day-of-week dynamics tell a tale of two opposite forces. Travelers opted to stay home for Mother’s Day, putting a damper on weekend occupancy, which was down 4.7 percentage points (ppts) week over week (WoW). Weekday occupancy, on the other hand, improved 2.4 ppts WoW as signs of increased business travel and weekday leisure travel emerging. Compared to last year, occupancy showed a modest decline of 1.4 percentage points (ppts), impacted partially by the Mother’s Day calendar shift making this year a harder comp to last year with Mother’s Day occurring one week earlier in 2022.

- Average daily rate (ADR) at US$155 was US$2.70 lower than the prior week and a 3.4% increase year over year (YoY). The increase was just behind the most recent CPI-indexed annual inflation rate (5.0%).

- With slightly weaker ADR, revenue per available room (RevPAR) fell US$1.90 week over week (WoW) to US$101.

- Comparing the past four weeks to the matching period last year, all indicators were positive with occupancy up 0.4 ppts, ADR up 4.9% and RevPAR up 5.4%. This points to a possible repeat of the “summer of summers” experienced last year as the Memorial Day holiday and the unofficial kickoff to summer travel season is just weeks away.

Top 25 Markets vs. the rest of the country

The U.S. Top 25 Markets finished the week at 70.6% occupancy, down slightly from a week prior (-0.4 ppts WoW). Markets outside of the Top 25 held steady WoW at 62.1%. ADR in the Top 25 Markets declined 2.3% WoW to US$187 while all other markets experienced a smaller decline (-1.1%) to US$136. The muted performance on the weekend due to Mother’s Day impacted the overall performance.

Monday through Wednesday occupancy for the Top 25 Markets increased 2.3 ppts WoW to 72.6%, while Friday through Saturday occupancy declined 2.7 ppts to 76.0%.

The top market performer once again owes thanks to the Taylor Swift stadium tour as Philadelphia, hosting the star over the weekend, posted the Top 25’s largest WoW increases in occupancy (+8.8 ppts), ADR (+27.1%) and RevPAR (+44.5%). Philadelphia weekend occupancy and ADR was 89.1% and US$253, not quite as high as the previous week in Nashville. Music City saw weekend occupancy and ADR of 94.2% and US$318 respectively. The Taylor Swift tour moves to Boston followed by East Rutherford and Chicago.

Washington, D.C. and Denver were the next two top performers with WoW RevPAR increasing 19.4% and 14.0%, respectively. New York City continued to hold the top occupancy, ADR and RevPAR positions among the Top 25.

Segmentation

Group bookings at luxury and upper upscale hotels dropped 9.4% WoW as the spring convention season slows. Group bookings essentially matched last year’s levels (-0.4%); however, the Mother’s Day shift made for a harder comp this week as noted above. Transient bookings at luxury and upper upscale hotels increased 5.1% from the prior week and were 3.6% above last year’s levels, seemingly less impacted by Mother’s Day. Perhaps some travelers decided to pamper mom with a hotel stay.

- The majority of the Top 25 Markets (15 of 25) experienced a WoW transient increase, while on the group side, the majority (16 of 25) experienced a WoW group decrease.

- The strongest group markets week over week were Detroit, Las Vegas, and Washington, D.C.

- The strongest transient markets week over week were Denver, Minneapolis, and Philadelphia.

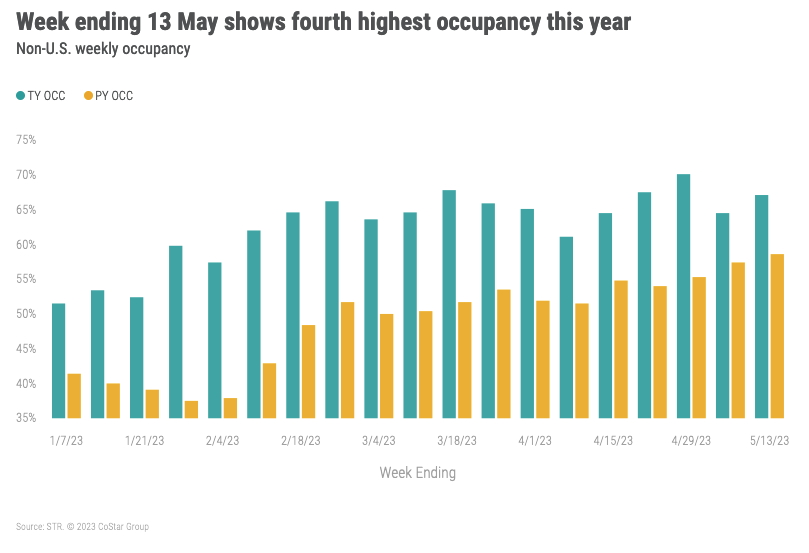

Global Performance

The gap between 2022 and 2023 global occupancy (excl. U.S.) has been closing as the effects of the last major wave of COVID receded this time last year. The occupancy difference between this year and last year sits comfortably in single digits, +8.5ppts this week and last week even closer at +7.1 ppts. Weekly ADR came in 17.8% higher YoY at US$137, decreasing slightly from the previous week by 7.4%. Resulting RevPAR for week was US$92.

Occupancy for the top 10 countries by total supply came in at 69.3% which was slightly higher than the aggregate of the other countries around the world excluding the U.S. (63.7%). Huge recoveries can be seen across many of the countries that last year had restrictions in place.

- China continues to grow, increasing occupancy 23.3ppts YoY after posting a 19.9ppt gain the week before.

- The story for Germany points to great improvements in the last couple of months with this most recent week producing the second highest occupancy (76.5%) of the top 10 countries.

- France saw a small decline in occupancy compared to the same week last year (-2 ppts). This in part could be attributed to the school holidays, which were the last to end for Zone C (which includes Paris) on Monday, 8 May. Strikes across at the country have shown only limited impact on performance.

The UAE continued to outperform all top 10 countries with occupancy at 81.8%, however, now past Ramadan and Eid al-Fitr comparisons, there is evidence of some rate growth slowdown. ADR was US$167.68, down 12.6% from the comparable week last year.

Final thoughts

Both U.S. and global results were impacted by normal seasonal slowing. Leisure travel remains strong, group is slowing as spring convention seasons wanes, and business/corporate improves as we see continuing gains in weekday occupancy, particularly in the larger markets. ADR remained firmly grounded with positive annual gains, although the rate of ADR and RevPAR growth is moderating and will continue to do so.

Looking ahead

Performance next week is expected to pick up across the globe as we near the unofficial Memorial Day summer kickoff. College graduations will add to family travel, and as school districts in certain regions of the country start to let out, leisure travel will strengthen. Strong weekday performance provides the confidence to expect business transient travel will continue improving.

This article originally appeared on STR.